Canada needs to scale-up its defence spending to strengthen national resilience, allied security

‘Canada needs a defence scale-up that is not only larger but calibrated to avoid displacing investment that could better strengthen both national resilience and allied security,’ writes Rebekah Young. / SCOTIABANK PHOTO

Canada has little choice but to scale up its defence efforts. The world is more polarized, conflict risk is higher and sovereignty risk has itself been weaponized, exposing the costs of decades of underinvestment and visible capability gaps at home. The question is no longer whether Canada should do more, but how to do more in a way that strengthens both security and long-run resilience.

The security lens has also widened — likely permanently. The Iran war has demonstrated that energy systems, critical minerals, strategic infrastructure and supply chains are no longer adjacent economic considerations. They are part of the security architecture itself. NATO’s new 5% target moves in the right direction by recognizing a broader set of defence-enabling investments under its 1.5% bucket, even if the exact contours of that category are still being worked out.

Many of these related investments (energy, critical minerals, infrastructure, and upstream industrial capacity) should be economically and strategically valuable in their own right. Canada is already operating near this broader effort level and has both the ambition and resource base to go further. For Canada, the bigger issue may not be what qualifies under the 1.5% umbrella, but whether the target structure encourages further strategic investment or unintentionally constrains it in areas where Canada has a clear comparative advantage.

This argues for a defence scale-up that is not only larger but calibrated to avoid displacing investment that could better strengthen both national resilience and allied security.

From catch-up to scale-up

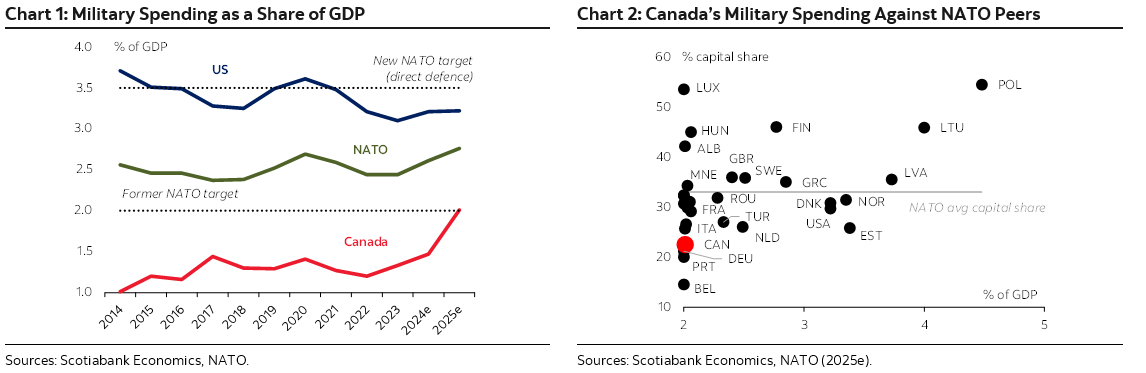

Canada is still digesting a rapid ramp-up in military outlays to meet NATO’s 2% target (charts 1 and 2). It was one of the last NATO members to meet the alliance’s earlier benchmark, and even that required a sharp near-term increase in spending. Fiscal-year 2026 (F26) defence outlays were lifted to about $63 billion — roughly 20% above plan and over 50% relative to $41 billion the year prior (cash basis) — with part of the increase delivered through an immediate pay raise for military personnel. Budget 2025’s net $81.8 billion (cash) allocation broadly sustains spending around the 2% threshold over the planning horizon.

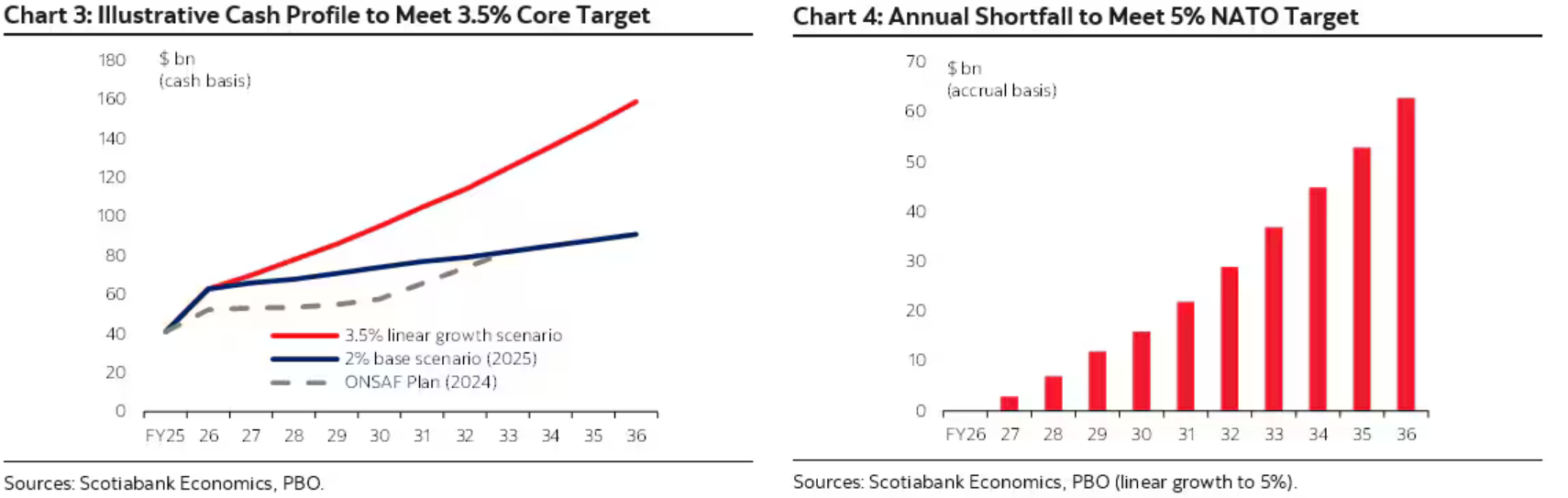

Getting to 5% would carry a very high price tag. The new NATO benchmark raises the direct defence spending target to 3.5% by 2035, along with a new 1.5% target for broader defence-related investments. The federal government has indicated that Canada likely already meets the 1.5% threshold but has not yet released a detailed fiscal plan. The Parliamentary Budget Officer (PBO) estimates that closing the gap could amount to another $68 billion (~ 1.5 % of GDP) annually above baseline by FY36—or a total annual outlay of $159 billion (cash) that year (charts 3 and 4).

The next phase will be even harder as Canada must simultaneously scale and reorient defence spending toward capital investment. It trails NATO peers against the alliance’s less-discussed compositional guidance to devote at least 20% of expenditures to major equipment, including related R&D. Canada has nearly doubled its equipment share over the past decade to 22.6% in 2025, but that remains well below the roughly one-third share of allies. Personnel, operating, and sustainment costs remain heavy, especially as aging fleets become more expensive to maintain, while infrastructure spending has remained persistently weak.

Meeting 5% would not just be a spending question, but also a financing one. A largely deficit-financed path would materially add to public debt and risk eroding Canada’s relative fiscal advantage, especially if spending fails to deliver expected growth gains. The PBO estimates this path could lift federal debt by more than 6 ppts by 2035. Before accounting for any dynamic impacts, that would put deficit and debt on markedly looser trajectories. Otherwise, a combination of higher taxes and/or spending restraint would foot at least part of the bill. IMF cross-country work has found that, in practice, about two-thirds of large defence buildups are typically financed through borrowing with the balance through fiscal adjustment.

Piecing together a coherent baseline — let alone a path to scale — is admittedly challenging. It requires assumptions about capital versus operating, cash versus accrual, defence versus related spending, federal versus provincial spending and what was already planned versus newly announced. Importantly, it also requires assumptions about growth, since the NATO target is defined as a share of GDP, which the spending path itself can influence.

The federal government will eventually need to spell out the path, but the picture today likely points to direct defence spending remaining uncomfortably close to 2% — at a time of mounting U.S. pressure. Even at that level, rebalancing toward higher capital spending would still look ambitious— and risky. Canada has yet to have these conversations.

Turning defence spending into domestic capacity

A bigger defence budget does not automatically translate into stronger domestic growth. The economic payoff depends on where the money goes (personnel, domestic sustainment, infrastructure, or imported equipment). Currently, roughly 55% of Canada’s defence supply chain is Canada-based, for example. In GDP terms, the rest leaks abroad rather than showing up as Canadian output.

Recent IMF empirical work reinforces the point. Defence buildups often begin as demand shocks, but their macro effects vary widely. Spending that is import-heavy or runs ahead of domestic capacity can drive inflationary pressures, weaken fiscal and external balances, and raise debt levels, while spending that is sustained, domestically captured, and capacity-building tends to generate stronger multipliers.

The ideal economic path converts fiscal effort into both capability and productive capacity. That means prioritizing spending that deepens the capital stock, strengthens firm capacity, builds labour skills, expands infrastructure, supports R&D, retains intellectual property, and opens export channels. By contrast, an operationally led expansion may support near-term activity, but is less likely to raise potential output and more likely to intensify fiscal, inflationary, and opportunity-cost pressures.

Canada’s new defence strategy broadly aligns with this logic. It shifts the focus from procurement to defence-industrial capacity, making domestic value capture the core economic test. Its Build–Partner–Buy framework operationalizes this approach: Build where Canada can develop sovereign capability; partner where scale, technology, or interoperability require it; and buy abroad only where necessary, ideally in ways that still strengthen Canadian firms, IP, sustainment, and control. New institutions, including the DIA and a Canada-based multilateral DSRB would help implement that strategy.

If it is well executed, such a defence ramp-up could strengthen both military capability and industrial capacity in sectors where sovereignty and productivity overlap.

Beyond the 5% benchmark

Canada’s implementation challenge also points to a broader alliance question. NATO needs not only more spending, but stronger coordination of effort across allies. The new 5% target is directionally right, but the 3.5%/1.5% split may be too rigid if it treats broader security investment as a capped residual rather than a strategic contribution.

Nor should the 3.5% bucket reflect a legacy view of rearmament alone. Core platforms still matter, but modern warfare is increasingly multi-domain, shaped by drones, sensors, satellites, cyber resilience, data, and integrated air and missile defence alongside traditional assets. A target structure that favours heavier spending on legacy platforms risks conflating volume with relevance. The alliance needs more military capability, but also the right mix—spending that is faster to field, better matched to the threat environment, and more effective in strengthening deterrence and industrial capacity.

Energy weaponization has moved from risk to reality since that target was set less than a year ago. Energy security, critical minerals, resilient infrastructure, and supply chains are now integral to military readiness and industrial resilience, not adjacent. NATO should keep core military capacity as the anchor, but its 5% framework should be flexible enough not to crowd out investments that may do more to strengthen national resilience and allied security. It should also leave allies room to contribute where they add the most strategic value.

For Canada, that means pressing for a framework that better recognizes investments in energy, minerals, Arctic infrastructure, ports, grids, and resilient supply chains, and ensures the 1.5% bucket functions as a floor for strategic investment, not an effective ceiling in a world of fiscal constraints, implementation bottlenecks, and hard choices.

NATO’s 2029 review is a natural checkpoint, but the case for that conversation may come sooner.

Move fast, spend well, think broad

Canada must move quickly, but it must also move tactically. In a more dangerous world, a larger defence effort is unavoidable. The real test is whether scarce fiscal room is translated into military capability, domestic capacity, and long-run resilience — not simply a higher spending ratio. Canada should scale core defence spending as quickly as credible absorption allows, while pressing NATO to ensure its 5% framework acts as a catalyst for high-value strategic investment, rather than a rigid structure that crowds out the very investments that could leave Canada and its allies stronger and more resilient.

This op-ed was originally published on Scotiabank’s website and reprinted with permission. It was edited for length.